Florida's 25% Roof Replacement Rule: The Critical 2026 Update Every Homeowner Must Understand

Florida's 25% Roof Replacement Rule: The Critical 2026 Update Every Homeowner Must Understand

Florida's 25% Roof Replacement Rule has shifted from a rigid mandate often requiring a full roof replacement to a more flexible code. This change, effective late 2023, now allows for repairs on certain code-compliant roofs, but creates a critical new conflict between what the building code permits and what homeowners insurance carriers demand for coverage.

The Eye of the Storm: Why a Simple Rule Became a Homeowner's Nightmare

Imagine the scene: a hurricane has just passed. The winds have subsided, and you step outside to assess the damage. You find a section of your roof has lost shingles—not the whole thing, but a significant patch. In the past, this scenario would trigger a cascade of events dictated by one of the most consequential—and controversial—sections of the Florida Building Code: the 25% Rule. For years, this rule was a primary driver in the state's escalating property insurance crisis, a seemingly simple regulation with profoundly expensive consequences for homeowners.

At Roof Bear, our GAF Master Elite® certified team has spent decades on the front lines, navigating the complexities of Florida's unique roofing landscape. As a Top 1% Veteran-Owned company, we believe in precision, integrity, and providing homeowners with the unvarnished truth. The recent changes to the 25% Rule are significant, and understanding them is no longer just about code compliance; it's about protecting your home's long-term financial health and insurability.

Deconstructing the 'Old 25% Rule': A Well-Intentioned Code with Unintended Consequences

To grasp the magnitude of the recent changes, we must first understand the rule that governed Florida roofing for years. The original intent was sound: to ensure that when a roof undergoes significant work, the entire system is brought up to modern, safer building standards. This prevents a patchwork of old and new materials that could compromise the roof system integrity during the next storm.

The specific language was clear and unforgiving. The previous '25% Rule' stated: 'Not more than 25 percent of the total roof area or roof section of any existing building or structure shall be repaired, replaced or recovered in any 12-month period unless the entire existing roofing system or roof section is replaced to conform to requirements of this code.' In practice, this meant that if an insurance adjuster or a licensed roofing contractor determined that more than a quarter of your roof had sustained damage, you weren't looking at a simple roof repair. You were legally required to undertake a full roof replacement.

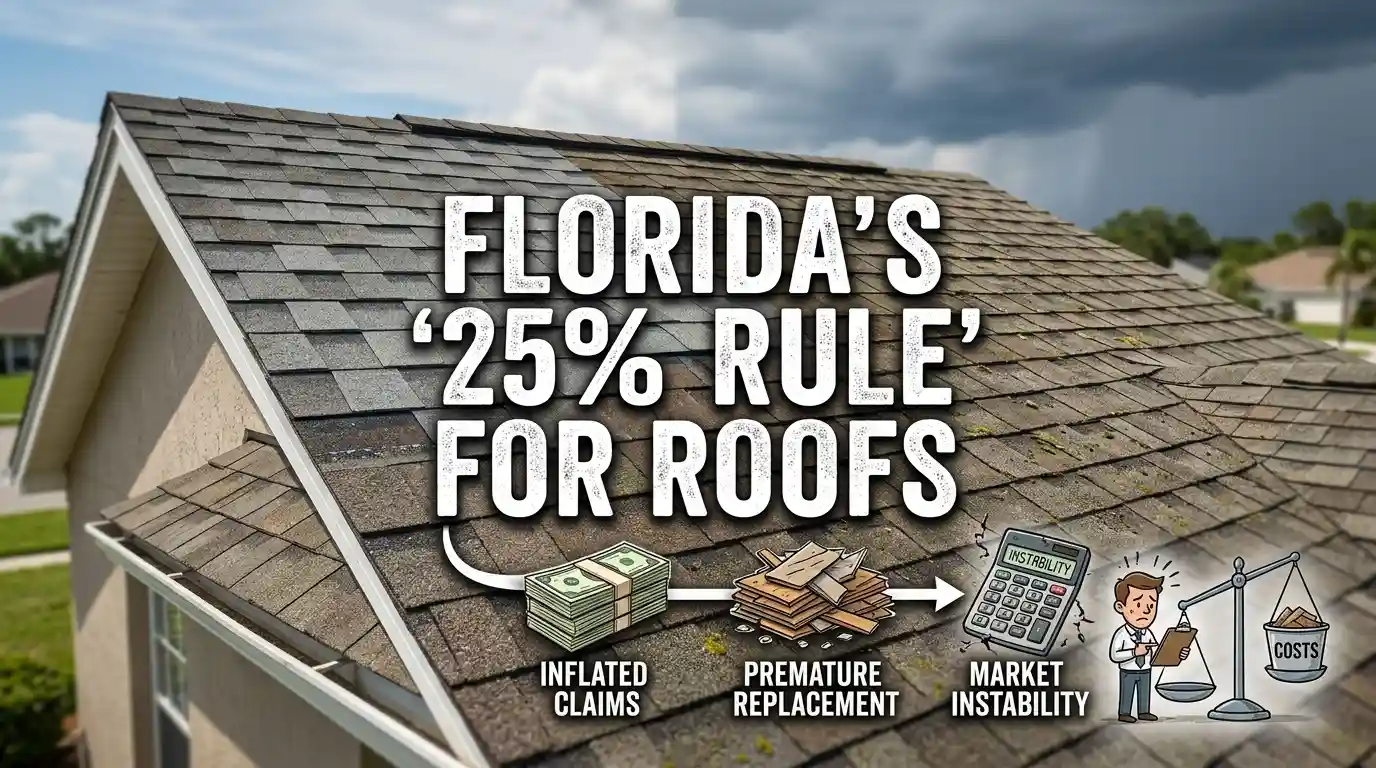

For homeowners, this often felt like a punitive measure. A section of wind damage that might cost a few thousand dollars to repair could trigger a mandatory $20,000, $30,000, or even $40,000 full replacement. This created a perfect storm for the insurance market:

- Inflated Claims: What should have been minor property damage claims ballooned into massive replacement cost value (RCV) payouts.

- Premature Replacements: Perfectly good sections of roofing, often 75% of the entire roof, were being torn off and sent to landfills simply because of a localized area of storm damage.

- Market Instability: Insurance carriers, facing staggering losses from these inflated claims, began to raise insurance premiums dramatically, pull out of the state, or become insolvent. This pushed hundreds of thousands of homeowners into the state-backed insurer of last resort, Citizens Property Insurance Corporation.

This well-intentioned code, designed to improve safety, inadvertently became a key driver of the Florida home insurance crisis. It removed nuance from the damage assessment process and forced a one-size-fits-all solution that was financially unsustainable for both homeowners and insurers.

The Game Changer: How Senate Bill 4-D and the 2023 FBC Rewrote the Rules

The Florida Legislature, facing an untenable insurance market, took decisive action. Through a series of property insurance reform bills, culminating in changes reflected in the new building code, they directly addressed the 25% replacement rule. The most significant shift arrived with the official adoption of the updated code. The effective date for the most recent major update, the Florida Building Code, 8th Edition (2023), was December 31, 2023.

This new edition introduced a critical exception into the Florida Statutes governing roof repair vs. replacement. The law no longer contains the rigid 25% mandate for many homes. Here is the crucial change:

The New Exception: If an existing roof system was installed in compliance with the 2007 Florida Building Code or any subsequent edition, and more than 25% of the roof is damaged, the law now allows for the roof to be repaired, provided that matching roofing material is available. This effectively eliminates the automatic trigger for a full roof replacement that existed under the old law.

This is a fundamental shift in philosophy. The state is moving away from a prescriptive mandate and toward a more flexible approach. However, that "if" is doing a lot of work. "Compliance with the 2007 FBC" is a technical standard. It generally means the roof has a proper secondary water barrier (modern roof underlayment) and was installed to the code specifications of its time. Most asphalt shingle roofs, tile roofs, and metal roofs installed since 2007-2008 likely meet this requirement. Roofs older than that often do not, which means they may still fall under the old logic.

This change was intended to reduce the number of unnecessary full roof replacements, lower the cost of claims, and, hopefully, stabilize the insurance market. But in solving one problem, it created a complex new dilemma for property owners.

The New Homeowner's Dilemma: Navigating the Code vs. Coverage Conflict

The overhaul of the 25% rule has created a dangerous gap between what the building code *allows* you to do and what your insurance carrier will *demand* you do to maintain coverage. This is the new crux of the issue: just because you can legally repair your roof doesn't mean your insurer will agree to keep your policy active if you do.

Insurance companies are in the business of managing risk. An older roof, even one that has been repaired, represents a higher risk of future claims, water intrusion, and failure during the next hurricane. Carriers are increasingly using the age of roof as a primary factor for determining eligibility and setting insurance premiums. Many are refusing to write new policies for homes with roofs over 10-15 years old, regardless of condition.

This creates a critical conflict. After a storm, you now face a choice with significant long-term consequences. Let's break down the new landscape:

The Old, Rigid '25% Rule' Mandate

- Pros: The path was clear, albeit expensive. A determination of over 25% damage led directly to a new, fully code-compliant roof. This satisfied both the building inspector and the insurance company, guaranteeing future insurability.

- Cons: The cost was often astronomical, forcing homeowners to pay large deductibles for a replacement they didn't feel they needed. It fueled market instability and led to a massive waste of serviceable roofing materials.

The New Homeowner Decision-Making Responsibility

- Pros: You now have the flexibility to opt for a much less expensive roof repair, potentially saving you thousands of dollars out-of-pocket, especially if you have a high insurance policy deductible or an actual cash value (ACV) policy that depreciates the value of your old roof.

- Cons: This choice introduces significant uncertainty. Your insurance carrier may see the repaired, aging roof as an unacceptable risk and choose to non-renew your policy, leaving you scrambling for coverage. The repair, while legal, may be a temporary solution that costs you more in the long run through higher premiums or a future forced replacement on your own dime.

You might save money today by choosing repair, only to receive a non-renewal notice in six months. This forces you into a far worse position: trying to find a new insurance policy with a roof that no standard carrier wants to cover, pushing you toward the expensive and limited options offered by Citizens. The short-term win can easily become a long-term strategic loss.

Beyond the 25% Exception: When a Full Roof Replacement is Still Mandatory

It's crucial to understand that the new flexibility has limits. The 25% rule hasn't been completely eliminated; it has been amended with specific exceptions. There are still clear scenarios where a full roof replacement is not just the best option, but the only legally permissible one. A building permit is required for this work, and a building inspector will enforce these requirements.

A full roof replacement is still required under the Florida Building Code if any of the following conditions are met:

- The 50% Threshold: If more than 50% of the total roof area is damaged, a full replacement is mandatory. The 25% exception does not apply in cases of such extensive damage.

- Pre-2007 FBC Non-Compliance: If your existing roof was not installed to the standards of the 2007 Florida Building Code (or later), the old 25% rule logic essentially still applies. An older roof without a sealed underlayment or proper decking attachment will trigger a replacement if more than 25% is damaged. This primarily affects roofs installed before 2008.

- Substantial Structural Damage: The rules for repair versus replacement primarily concern the roof covering (shingles, tile, metal). If the underlying roof decking or structural supports have significant structural damage, those sections must be replaced to meet current code, which often makes a full replacement the only practical and safe option.

- Material Mismatch: The exception allowing for repair is contingent on the availability of matching roofing materials to maintain a uniform appearance. If your specific shingle or tile is no longer manufactured, and a suitable match cannot be found, a building official may still require a full replacement of the affected roof section to avoid a patchwork look, which can violate local ordinances or HOA rules.

- High-Velocity Hurricane Zone (HVHZ) Rules: The regulations for Miami-Dade and Broward County are often stricter than the base Florida Building Code. Homeowners in the HVHZ should always consult with a local, licensed roofing contractor who is an expert in the specific and more rigorous requirements of that zone.

The code is very specific about what constitutes a replacement. The Florida Building Code defines 'ROOF REPLACEMENT' as 'The process of removing the existing roof covering, repairing any damaged substrate and installing a new roof covering,' distinguishing it from a 'ROOF RECOVER,' which involves installing a new layer over the old one—a practice now heavily restricted in Florida.

Key Factors in Your Repair vs. Replacement Decision

As a homeowner in Florida today, you are the decision-maker. This is a significant responsibility. At Roof Bear, our role is not to push you one way or the other, but to provide a comprehensive damage assessment and a clear explanation of the variables so you can make an informed choice. Here are the four critical factors you must weigh.

Immediate Out-of-Pocket Cost

A roof repair will almost always be the cheaper option upfront. If you have a $2,500 hurricane deductible and the repair costs $3,000, your out-of-pocket expense is manageable. A full $25,000 replacement, however, still requires you to pay that same deductible. For homeowners on a tight budget, or those with ACV policies that pay very little for an old roof, the immediate savings of a repair can be very appealing. As one of our clients noted after we identified an efficient repair strategy, "They did an amazing job !! It looks perfect and $1,600 savings". This highlights that in the right situation, a professional repair can be a cost-effective solution.

Impact on Future Insurance Premiums and Coverage Eligibility

This is the most critical long-term factor. Before you agree to a repair on an aging roof (e.g., a 15-year-old shingle roof), you should contact your insurance agent and ask for written confirmation that your policy will be renewed. Without this guarantee, you risk being dropped at your next renewal period. A new roof, conversely, makes your home highly attractive to insurers. It can secure you better coverage, lower insurance premiums, and qualify you for valuable wind mitigation credits that can save you hundreds of dollars per year.

Long-Term Resilience and Code Compliance

A full roof replacement provides a complete, integrated system built to the very latest building codes. This means superior roof underlayment, enhanced nailing patterns, and modern materials that offer far greater protection against wind and water intrusion. It is an investment in your home's resilience and your family's safety. One customer who made this investment told us, "So happy with my new Metal Roof , skylights and TPO flat roof! The Roof Bear crew was excellent, even going above and beyond to make things perfect." This speaks to the peace of mind that comes with a top-tier replacement. This proactive approach is also being mirrored in legislation; for example, new Florida regulations require condo associations to budget and collect sufficient reserves to cover the cost of replacing building components, specifically including roofs, underscoring a statewide focus on long-term structural integrity.

The Actual Extent and Nature of the Roof Damage

Not all damage is equal. A handful of missing shingles in one contiguous area is a prime candidate for a simple repair. However, widespread, non-contiguous damage, such as creased shingles across multiple roof facets, significant granule loss, or lifted tiles, indicates a systemic problem. In these cases, a repair is like putting a bandage on a broken arm. It might cover the visible issue, but it doesn't address the underlying weakness of the entire roof system, leaving you vulnerable in the next storm.

Expert Answers to Your Pressing Roofing Questions

Navigating a property damage claim can be confusing. As industry experts, we hear the same questions from concerned homeowners repeatedly. Here are straightforward answers to some of the most common ones.

How to Navigate Conversations with a Roof Insurance Adjuster

Your interaction with the insurance adjuster is a critical part of the claims process. What you say—and what you don't say—matters. Here is our advice on what not to say:

- Do Not Speculate: Don't say, "I think the leak started a few months ago," or "It looks like the wind really lifted these shingles." Stick to what you know. "I noticed a water spot on my ceiling on this date." Let the professionals determine the cause and timeline.

- Do Not Admit to Pre-Existing Damage: Never volunteer information about previous leaks or known issues with the roof unless specifically asked. Your claim should focus only on the new damage caused by the recent event (e.g., the hurricane).

- Do Not Agree to a Recorded Statement Immediately: You have the right to understand your policy and the situation before giving a formal statement. It's perfectly acceptable to say you need to review your policy and speak with your roofing contractor first.

- Do Not Accept the First Offer Without Review: The adjuster's initial damage assessment and settlement offer may not be complete. It is highly recommended to have a trusted, licensed roofing contractor review the adjuster's scope of work to ensure nothing was missed. A public adjuster can also be an advocate on your behalf.

Is There a "Cheapest" Time of Year for a New Roof?

In many parts of the country, roofing has a distinct on- and off-season. In Florida, the calculus is different. Our "season" is dictated by hurricanes. The busiest, and therefore often most expensive, time to get a roof replaced is immediately following a major storm, when demand skyrockets and resources are stretched thin. The "cheapest" time is typically during the drier, milder months from late winter to early spring (February through April), before the storm season ramps up. However, the primary consideration should always be protection. Waiting for a slightly better price could mean leaving your home vulnerable when the next storm forms in the Atlantic. The best time for a new roof is when your old one is no longer providing adequate protection.

Red Flags: How to Tell if a Roofer is Lying

Unfortunately, the aftermath of a storm can bring out unscrupulous actors. As a homeowner, you must be vigilant. Here are clear red flags that indicate a roofer may not be trustworthy:

- High-Pressure Sales Tactics: A reputable contractor will provide a detailed estimate and give you time to consider it. Anyone demanding an immediate decision "before the offer expires" is a major red flag.

- "We Can Eat Your Deductible": Any roofer who offers to waive or absorb your insurance deductible is proposing to commit insurance fraud. This is illegal and could have serious consequences for you as the homeowner.

- Lack of Proper Credentials: Always ask for proof of state licensing and liability/workers' compensation insurance. Verify their license on the Florida Department of Business and Professional Regulation (DBPR) website. A contractor who can't provide these is not legitimate.

- Vague Contracts: A proper contract will detail the specific materials to be used (brand, color, type), scope of work, timeline, and total cost. If the contract is vague, walk away.

- Demands for Large Upfront Payment: While a deposit for materials is standard (typically 10-30%), a roofer demanding a majority of the payment before work begins is a significant risk.

- Use of Subcontractors: Ask if they use their own employees. At Roof Bear, we pride ourselves on our 100% In-House Roofing Team. This ensures accountability, consistent quality, and clear communication—no mystery crews showing up at your door.

Making the Right Choice for Your Needs

The right decision on repairing or replacing your roof depends entirely on your personal financial situation, your tolerance for risk, and your long-term goals for your home. There is no longer a single "correct" answer. Here is our tailored advice for different types of homeowners:

-For the Budget-Conscious Homeowner

If you have recent, localized storm damage and your primary focus is the lowest immediate cost, a repair is a viable option under the new law. However, you must do your due diligence. Before proceeding, get written confirmation from your insurance carrier that a repair will not jeopardize your policy renewal. If they won't provide it, the short-term savings from a repair could be wiped out by the long-term cost of being forced into a more expensive insurance policy or having to pay for a full replacement later without any insurance assistance.

-For the Risk-Averse Planner

If your priority is long-term home value, resilience against future storms, and maintaining affordable, comprehensive home insurance, a full roof replacement is the wisest investment. It resolves the immediate damage while eliminating the significant risk of being dropped by your insurer. A new, code-compliant roof lowers your home's risk profile, often leading to lower premiums and ensuring you have robust coverage when the next storm hits. It is the definitive solution for peace of mind.

-For the Uninsurable Homeowner

If you have already been dropped by your insurer or are facing a massive premium hike specifically because of the age or condition of your roof, your path is clear. A repair will not solve your core problem. Your primary goal is to make your home insurable again in the standard market. A full, professionally installed, and properly permitted roof replacement is the most direct—and often the only—way to achieve this. It is the key to escaping the high costs and limited coverage of last-resort policies and regaining control over your home's financial stability.

The seismic shift in Florida's 25% Rule is more than a building code update; it's a transfer of responsibility. The decision, and its consequences, now rest squarely on your shoulders. As a GAF Master Elite® contractor and a veteran-owned business, we believe our mission is to arm you with the expert knowledge and honest assessment you need to make that decision with confidence. Our 100% In-House Roofing Team is committed to delivering quality and transparency, ensuring the solution you choose is the one that best protects your home and family. For a comprehensive, no-obligation roof inspection and a clear breakdown of your options, we encourage you to contact our team of experts serving homeowners across Orlando, FL, and the surrounding Central Florida region.